The Hidden Insurance Gaps for Rideshare and Delivery Drivers

Driving for these services on your regular car insurance is not allowed. If your car is damaged while driving for the app, your private insurance company can legally refuse to pay the claim. What’s the solution: call and ask for a rideshare or delivery insurance rider. It doesn’t cost much and fills in the gaps in coverage.

The growth of the gig economy has created flexible income opportunities for millions of Americans. Services such as DoorDash, Uber Eats, and TaskRabbit connect drivers with customers who want food delivered, errands run, or odd jobs completed on demand. Yet one issue remains persistently misunderstood: auto insurance coverage gaps. Many drivers assume their personal insurance or the platform’s coverage will protect them if something goes wrong. In reality, both assumptions are often false.

The growth of the gig economy has created flexible income opportunities for millions of Americans. Services such as DoorDash, Uber Eats, and TaskRabbit connect drivers with customers who want food delivered, errands run, or odd jobs completed on demand. Yet one issue remains persistently misunderstood: auto insurance coverage gaps. Many drivers assume their personal insurance or the platform’s coverage will protect them if something goes wrong. In reality, both assumptions are often false.

This post will explain how and why these gaps arise, and give examples of situations where (1) drivers find themselves without insurance for their own damaged vehicles, and (2) third parties injured in an accident may find no accessible liability insurance at all.

1. Why Personal Insurance Often Fails Drivers

Most standard personal auto insurance policies exclude business use of the insured vehicle. That means when a driver is delivering meals or performing tasks for compensation, the insurer can deny coverage. For many drivers, the first time they learn about this exclusion is after an accident.

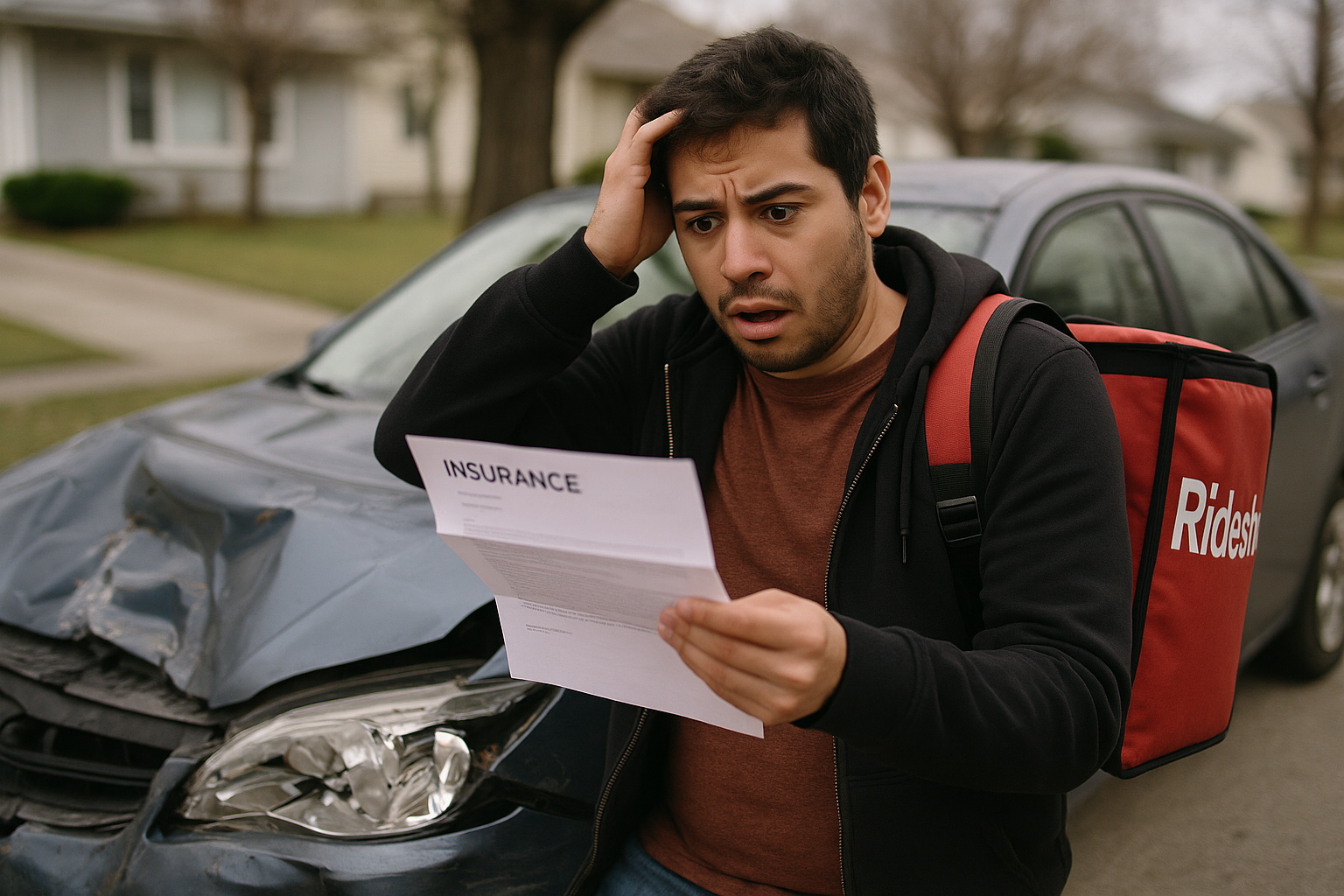

Consider Emily, a part-time delivery driver for DoorDash. On a rainy night she slides off the road and collides with a guardrail, causing $6,000 in damage to her car. Emily files a claim with her personal insurer, but the company denies it, citing the “livery” or “commercial use” exclusion. She then turns to DoorDash, only to discover that the platform’s insurance covers third-party liability only — not damage to her own vehicle. The result: Emily must pay for the repairs herself.

This is not a rare occurrence. Unless a driver has purchased a commercial auto policy or a special rideshare/delivery endorsement, there is no coverage for their vehicle while they are on the job.

Takeaway? Buy a rideshare endorsement for your personal policy if you are driving for any of these services or you are likely going to be out of luck in a crash.

2. Limited Platform Coverage Leaves Gaps

Some platforms, like Uber Eats, do provide contingent collision coverage — but only if the driver already carries collision coverage on their personal policy, and usually with a high deductible (often $2,500). If the driver does not maintain that coverage personally, Uber provides nothing.

By contrast, DoorDash provides no such contingent coverage at all. The driver’s car is never insured for physical damage through the platform. TaskRabbit offers no auto insurance whatsoever, noting that its “Happiness Pledge” is not insurance and does not apply to vehicle accidents.

This leads to a common misconception: while drivers believe they are “insured” through the app, that coverage usually applies only to other people’s injuries or property damage. The driver’s own car is, more often than not, left uninsured.

3. When Third Parties Can’t Recover

The insurance gaps don’t only affect drivers. Sometimes third parties injured in accidents discover that neither the driver’s personal insurer nor the platform’s policy will cover their claims.

Take John, who uses his personal car to perform handyman errands through TaskRabbit. While rushing to pick up supplies for a job, he rear-ends another vehicle at an intersection. The other driver, Susan, suffers neck injuries and faces significant medical bills.

- John’s personal policy denies the claim because he was using the car for business.

- TaskRabbit’s platform provides no liability insurance for drivers.

- Result: Susan must sue John personally to recover, and John’s assets may not be sufficient to cover her injuries.

In another example, imagine David, an Uber Eats driver whose personal auto policy has lapsed because he could not afford the premiums. While delivering food, he runs a red light and causes a serious accident. Uber’s contingent liability coverage generally applies only when the app is “on” and the driver is actively engaged in delivery — but if the driver’s personal policy is nonexistent or canceled, the claims process may stall or result in litigation. Meanwhile, the injured third parties face uncertainty about who will actually pay their damages.

4. Practical Lessons for Drivers and Victims

The key lesson is that gaps exist both ways:

- Drivers may find themselves without coverage for their own losses.

- Third parties may find themselves without access to insurance, forced to chase an underinsured or uninsured driver directly.

Drivers should not assume the apps’ policies will fill the void. Instead, they should:

- Review their personal auto policy for “business use” exclusions.

- Get with with their insurer about rideshare or delivery endorsements.

- Consider the cost of commercial auto coverage if driving is a significant source of income.

Third parties injured in gig-related accidents should consult counsel promptly. Recovery may depend on navigating layered policies, determining whether the platform’s coverage applies, and evaluating the driver’s own insurance status.

5. Policy Debate and Uncertain Future

Courts and regulators are increasingly scrutinizing these arrangements. Some states have mandated clearer disclosures from rideshare companies, but delivery platforms remain less regulated. Until there is broader reform, drivers and accident victims alike must be cautious and proactive.

The Future

The promise of gig work is flexibility and extra income. But without the right insurance, that promise comes with hidden costs. Drivers risk being left without coverage for their own car, while accident victims may be left without a clear path to compensation. Both groups must navigate a system where responsibility is dumped on the least educated person in the group.

For gig workers and those who may encounter them on the road, the safest course is knowledge: understanding where coverage ends, where exclusions begin, and how to protect yourself before an accident happens.